Ready to seek assistance with your US taxes?

Filing US taxes as an American abroad is complex. We help make it easy for you.

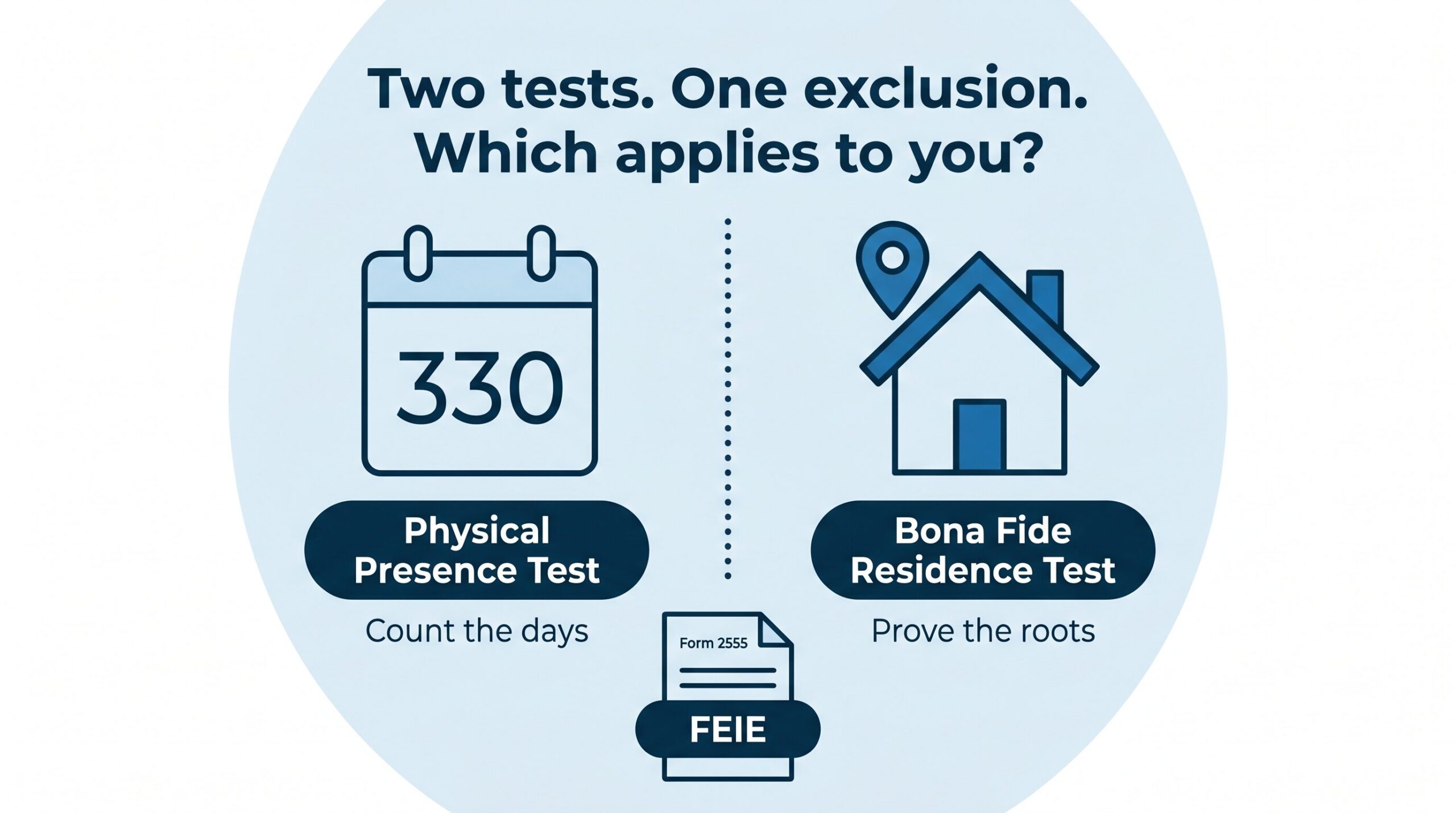

The Foreign Earned Income Exclusion can eliminate US federal income tax on up to $130,000 of income you earn abroad in 2025. To claim it, you need to qualify under one of two tests: the Bona Fide Residence Test or the Physical Presence Test.

They sound like they accomplish the same thing. Technically, they do. But they work completely differently, suit completely different situations, and fail in completely different ways. Choosing the wrong one, or misunderstanding what each actually requires, is one of the most common and costly mistakes Americans abroad make when filing their US return.

This guide explains how each test works, when each one is the better choice, the specific failure modes that catch people off guard, and a practical framework for deciding which one applies to your situation.

The Physical Presence Test takes a purely mathematical approach. It counts where you physically spent your time. To qualify, you need to be physically present in a foreign country for at least 330 full days during any consecutive 12-month period.

That 12-month period does not have to align with the calendar year. It can begin on any date and end 12 months later. This flexibility is one of the Physical Presence Test’s most useful features for people who moved abroad mid-year. You can start counting from the day you left and qualify for a prorated FEIE on your first partial year abroad before you have completed a full calendar year of foreign residency.

What counts as a “full day” is strict. A day counts only if you spent the entire 24-hour period outside the United States. The day you depart the US and the day you return do not count. A flight that touches down in the US, even briefly, removes that day from your count.

The 330-day requirement sounds simple, but it is the source of countless surprises. If you spend 36 days in the US in a 12-month period, you have 329 qualifying days. You fail the test. There is no partial exclusion. No grace period. No rounding. 329 days means no FEIE under this test for that period.

This is why careful day-tracking is non-negotiable if you are relying on the Physical Presence Test. A simple spreadsheet logging your travel dates, including the dates of every US entry and exit, is the minimum. Border crossing records, passport stamps, and flight receipts are your evidence if the IRS ever asks.

What the Physical Presence Test does not care about: your intent, where your home is, how long you plan to stay, what your visa status is, or whether you have ties to the foreign country. It asks only one question: were you physically outside the US for 330 days in this 12-month window?

The Bona Fide Residence Test takes a completely different approach. Instead of counting days, the IRS asks whether you are a genuine resident of a foreign country, someone who has established real roots there, not just someone temporarily working overseas.

To qualify, you need to be a bona fide resident of a foreign country for an entire calendar year. That means the test cannot be met in your first year abroad by itself. You must complete a full calendar year of foreign residency. However, once you establish bona fide residence, it applies retroactively to the beginning of your residency, which means you can claim the FEIE for partial periods in your arrival year and departure year.

What the IRS actually looks at is a facts-and-circumstances analysis with no single determining factor. The elements that carry the most weight include: whether you have a permanent place of abode in the foreign country, the nature of your employment or business presence there, whether your family is with you, your participation in the local community, whether you have a visa or permit for indefinite stay, whether you pay local taxes, and how you represent your residency on official documents.

Intent matters significantly. A US employee sent abroad on a fixed-term assignment with a predetermined return date, even if the assignment lasts two or three years, typically does not qualify for Bona Fide Residence because the intent was always to return. Someone who genuinely relocated, established a home, and has no fixed return date is a much stronger candidate.

The university professor example: We covered a real situation in our Reddit reaction video — a US professor teaching at a foreign university on a long-term contract, with foreign property, who spent three months back in the US for summer research. The question was whether that summer disrupted bona fide residence. The answer, based on the full facts, was likely no. A long-term faculty contract, foreign property, and a genuine home base abroad paint a picture of someone whose life is rooted in the foreign country, not someone temporarily posted there. The summer research trip was incidental to an established foreign residency. This is exactly the kind of analysis the Bona Fide Residence Test requires: facts-specific, not formulaic.

You moved abroad mid-year and need to claim the FEIE on your first partial year. The Bona Fide Residence Test cannot be fully established until you complete a full calendar year. The Physical Presence Test can qualify you as soon as you hit 330 days in any 12-month window, allowing a prorated FEIE in your first year.

You are a digital nomad or frequent mover. If you do not have a single foreign country you call home, establishing bona fide residence anywhere is difficult. The Physical Presence Test does not require a single country. You can split your 330 days across multiple foreign countries and still qualify, as long as none of those days were in the US.

Your residency status in the foreign country is uncertain. If your visa or permit situation is unclear, or if you are on a temporary work authorization, the Physical Presence Test avoids the question of whether your residency is legally established under the Bona Fide Residence standard.

You want a clear, auditable test. The Physical Presence Test produces a number. Either you hit 330 days or you did not. The Bona Fide Residence Test involves judgment and interpretation. For clients who want certainty and a clean paper trail, the day-count test eliminates ambiguity.

You travel to the US frequently. The Physical Presence Test’s hard 330-day requirement means frequent US visits can easily push you below the threshold. The Bona Fide Residence Test has no specific day-count requirement. As long as your foreign residency is genuine and your US time does not suggest you have relocated back, you can visit more freely without jeopardizing the exclusion.

You are established in one country for the long term. Someone who has lived in Germany for five years, owns property there, pays local taxes, and has no plans to return to the US is a textbook bona fide resident. Using the Physical Presence Test in this situation would be unnecessarily restrictive when the facts clearly support the stronger and more flexible test.

You moved abroad part-way through the year and want to establish residency from day one. Once bona fide residence is established at year end, it applies retroactively to the date your residency began. Combined with an extension to file your return until the residency is formally established, this allows you to claim the FEIE for the full period of your foreign residency in year one, potentially a better result than the Physical Presence Test’s prorated exclusion.

Your situation involves the IRS scrutinizing your residency. The Bona Fide Residence Test, while more subjective, builds a factual record of genuine foreign residency. For clients with complex situations, significant US income, US property, or frequent travel, the documented intent and established ties of bona fide residence can be a more defensible position than a day-count that was barely achieved.

The corporate assignment trap for the Physical Presence Test. An employee sent abroad on a fixed-term assignment often assumes they can use either test. The Physical Presence Test may be available since the day count is achievable. But if they are relying on the Bona Fide Residence Test, they often fail it precisely because the fixed end date signals that their residency was always temporary. This is one of the most common mischaracterizations we see on returns prepared by domestic CPAs who are not familiar with the distinction.

The 329-day cliff. There is no partial credit under the Physical Presence Test. Missing the 330-day threshold by a single day, one too many US trips or one transit stop that was longer than planned, eliminates the FEIE for that entire 12-month period. We have seen significant tax bills appear from a single unplanned US visit that pushed a client just below the threshold.

Assuming Bona Fide Residence is established automatically. Some expats assume that living abroad for several years automatically qualifies them under the Bona Fide Residence Test. It does not. If significant ties remain in the US, a home, a registered business, family, voter registration, the IRS may determine that the center of life never genuinely moved abroad. Establishing bona fide residence requires active documentation of foreign ties, not just the passage of time.

Switching tests without understanding the consequences. You can use different tests in different years depending on your circumstances. However, switching from the FEIE to the Foreign Tax Credit triggers the five-year revocation rule discussed in our FEIE vs FTC article. That rule applies regardless of which test you used to qualify for the exclusion. Switching the qualification test itself does not trigger the revocation rule, but it is worth understanding the interaction before making any changes.

Start with these four questions.

Did you complete a full calendar year abroad? If no, the Bona Fide Residence Test is not available for that year as the primary qualification. Consider the Physical Presence Test instead, or file an extension until the year completes.

How often do you visit the US? If more than 35 days per year on average, the Physical Presence Test becomes increasingly risky to rely on. Even one unexpected trip can push you below the threshold.

Is your foreign residency genuinely established, with a permanent home, local ties, and indefinite stay? If yes, the Bona Fide Residence Test is likely available and probably more flexible for your situation long-term.

Are you on a fixed-term assignment with a predetermined return date? If yes, the Bona Fide Residence Test will be difficult to establish regardless of how long the assignment runs.

Can I use both tests in the same year?

No. You only need to meet one test to qualify for the FEIE. You cannot use both simultaneously, but you can switch between years depending on your situation. Using a different test in different years is permitted and sometimes the right strategy, though any change should be considered in light of the FEIE revocation rule.

What counts as a “full day” for the Physical Presence Test?

A full day is a 24-hour calendar day spent entirely outside the United States. The day of departure from the US and the day of return to the US do not count as qualifying days, even if you spend most of those days abroad.

Does the Bona Fide Residence Test require a specific visa type?

No. Visa type is one of many factors the IRS considers but is not determinative. You can establish bona fide residence on a tourist visa in some circumstances, though it is harder to demonstrate without a long-term visa or work permit.

Can I qualify under the Physical Presence Test in my first year abroad?

Yes, if you can reach 330 days in a 12-month window that includes part of your first year abroad. The qualifying period can begin the day you leave the US and end 12 months later. If you reach 330 days within that window, you qualify for a prorated FEIE on the days that fall within the relevant tax year.

What happens if I fail the Physical Presence Test by one day?

You do not qualify for the FEIE under that test for that 12-month period. There is no partial exclusion and no grace period. If the Bona Fide Residence Test is available for that year, you may still qualify under that test instead. If neither test is available, the Foreign Tax Credit remains an option for reducing US tax liability on foreign income.

Does time in transit through the US count against the Physical Presence Test?

A transit through a US airport where you do not clear customs generally does not count as a US day. However, any day on which you are present in the US, even briefly after clearing customs, is not a qualifying day for the Physical Presence Test.

Which test applies to your situation depends on the specific facts of your residency, travel patterns, and income. This is one of the first questions we work through with every new expat client. Book a consultation and we will determine which test you qualify for and how to document it correctly.

Filing US taxes as an American abroad is complex. We help make it easy for you.