Ready to seek assistance with your US taxes?

Filing US taxes as an American abroad is complex. We help make it easy for you.

If you’re a US expat running or planning to run a business, how much tax you pay may depend on an important but often overlooked form: IRS Form 8832.

This form lets you choose how your business is taxed in the US, whether as a disregarded, pass-through entity, or as a corporation. Depending on the type of business, how many owners it has, and whether it’s registered in the US or abroad, filing Form 8832 can reduce your US tax reporting – and bill.

In this article, we take a closer look at Form 8832 – when to use it, how to file it, and why ignoring it can lead to unnecessary tax burdens and reporting headaches.

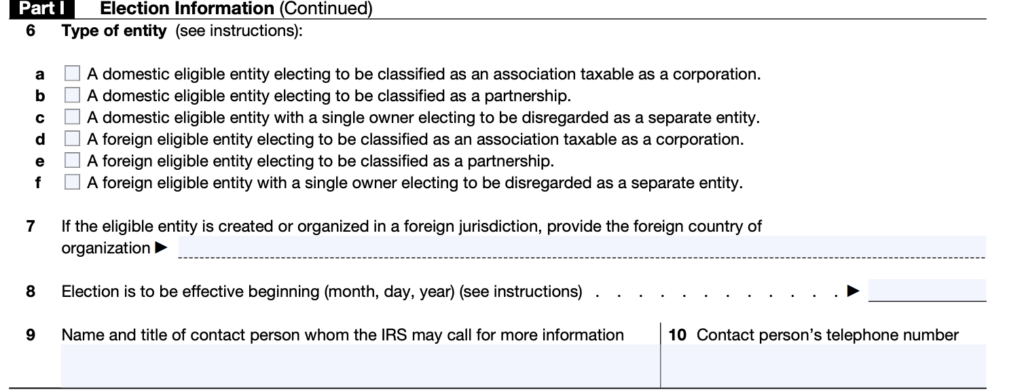

Form 8832 is used to make an Entity Classification Election, allowing eligible businesses to choose how they are taxed under US law—as a disregarded entity, partnership, or corporation. This gives expat business owners greater control over their US tax obligations. If Form 8832 isn’t filed, the IRS will assign a default classification, which may disadvantage you. Whether you’re setting up a new entity or wanting to change an existing entity’s status, Form 8832 lets you choose. If you don’t file it on the other hand, the IRS will assign a default classification based on ownership and location.

For example:

If you don’t file Form 8832, the IRS decides for you, and that may mean paying extra tax.

For US expats, Form 8832 isn’t just paperwork; it’s a strategic choice. Your business may be registered or operate abroad or in the US, but either way, the IRS might classify it in a way that is less than optimal for you. This could mean higher taxes and additional compliance obligations.

These can include:

or example, imagine you’re a US expat in the UK who sets up a UK private limited company (Ltd.)—a structure that offers limited liability similar to a US LLC. If you don’t file Form 8832, the IRS will automatically treat your company as a foreign corporation. This triggers complex reporting requirements, including Form 5471 and potential exposure to GILTI rules—even if you’ve already paid UK taxes. While you may be able to use foreign tax credits to avoid double taxation, you’ll still face additional costs and effort to stay compliant with the IRS. Filing Form 8832 can help you avoid these burdens by allowing you to choose a more favorable classification from the start.

The entity classification decision directly affects your tax liability, filing burden, and long-term planning flexibility.

Form 8832 is available to most entities that aren’t automatically treated as corporations under IRS rules.

Some foreign entities are always treated as corporations. The IRS keeps a list of these so-called “per se” corporations. If your entity is on that list, you cannot change its classification with Form 8832.

When you file Form 8832, you’re choosing how the IRS will tax your business entity. The options for US expats are disregarded entity, partnership, or corporation. Each choice comes with its own tax implications, reporting requirements, and long-term planning considerations—so it’s important to pick the one that best fits your situation and goals.

This option lets your business income flow directly onto your US return, typically on Schedule C or E, without filing a separate business return.

You’re eligible for the Foreign Earned Income Exclusion (FEIE) or the Foreign Tax Credit if you pay foreign taxes, but note that the FEIE can only be applied to income you earn, like salary or self‑employment pay, not on profits or distributions.

You’ll still owe self‑employment tax on all net earnings, and you won’t have legal liability protection.

Available for foreign entities with two or more US owners, this structure passes income directly to each partner’s tax return using Form 8865 for foreign partnerships. You gain flexibility in allocating profits and losses. However, you must handle extra disclosures like K-1s and complex international reporting.

Electing corporate status makes your business a separate taxpayer that files Form 1120 and pays a flat 21% US corporate tax. If it’s a foreign corporation, you’ll also need to file Form 5471, which can be complex and burdensome. This structure offers limited liability and lets you keep profits inside the business. However, you may lose expat tax benefits like the FEIE or FTC on retained earnings.

Once you make an election on Form 8832, it is generally binding for five years unless the IRS grants an exception. Given the long-term impact of this decision, it’s important to consult a US expat tax professional before filing.

Filing Form 8832 is relatively straightforward, but timing and precision are everything.

What you’ll need:

Yes, but only if you meet the conditions for late election relief. Otherwise, you may face IRS penalties. You must attach a signed, reasonable‑cause statement explaining the delay and affirming you acted reasonably and in good faith.

Form 8832 must normally be filed:

Approval isn’t automatic. If your request is denied or you don’t request relief, you could be stuck with the default classification.

Emma, a US expat living in Spain, sets up a Spanish S.L.—a type of limited liability company similar to a US LLC. Because she doesn’t file Form 8832, the IRS automatically treats the S.L. as a foreign corporation. This classification triggers a requirement to file Form 5471 annually, which Emma is unaware of. Two years later, she is assessed over $20,000 in penalties for failing to file. Had she timely filed Form 8832 to elect disregarded entity status, she could have avoided both the filing requirement and the resulting penalties.

Can I choose how my foreign business is taxed in the US?

Often, yes. Many foreign entities (like LLC equivalents) can file Form 8832 to be taxed as a disregarded entity, partnership, or corporation.

What happens if I don’t file Form 8832?

The IRS will apply default classification—often as a corporation, especially for “per se” entities—which may not match your tax strategy.

Why does my classification matter?

It impacts your US tax rate, reporting requirements, and whether you can claim benefits like the FEIE or Foreign Tax Credit.

Do I have to report foreign business income to the US?

Yes. US citizens must report all worldwide income, even if it’s already taxed abroad.

Form 8832 gives US expats the ability to choose how their foreign business is taxed under US law—offering greater control and potential tax savings. Taking the time to structure your business properly can prevent costly surprises later. Since the decision is hard to reverse, you should seek tax planning advice from an expat tax specialist as soon as possible.

Filing US taxes as an American abroad is complex. We help make it easy for you.